How easy (or hard) is to build a startup in Spain with the Startups Law 28/2022? (Part I)

Welcome to the #9 edition of How to Land in Venture Capital: a weekly newsletter of valuable pieces of research to help you land a job in VC, and some of the best VC Dealflow startup analysis.

I’m happy to have you here! Already +200 subscribers. Thanks!

In the today’s edition of How to land in Venture Capital, I want to give you a piece of research on the Spanish Startup Ecosystem that consist in three parts:

Part I: Spanish Startup Law 28/2022

Part II: Creating a startup Step by Step in Spain

Part III: Public funding in Spain: free money?

Today’s deep dive: Spanish Startup Ecosystem 1st part: Highlights of the New Startup Law 28/2022

The new Startup Law 28/2022, enacted on December 21, 2022, marks a significant step forward in Spain's efforts to foster a dynamic and innovative startup ecosystem. Let me guide through this law with this structure:

1. Startup Definition and Longevity

2. Fiscal Incentives

3. Regulation

Let’s start with the first point:

1. Startup Definition and Longevity

The new Law 28/2022 provides a clear definition of a startup in Spain. A startup is defined as an innovative company with a scalable business model that is less than 5 years old (or 7 years for strategic sectors like biotechnology, energy, and industrials). The company must not distribute dividends and must have its headquarters or a permanent establishment in Spain.

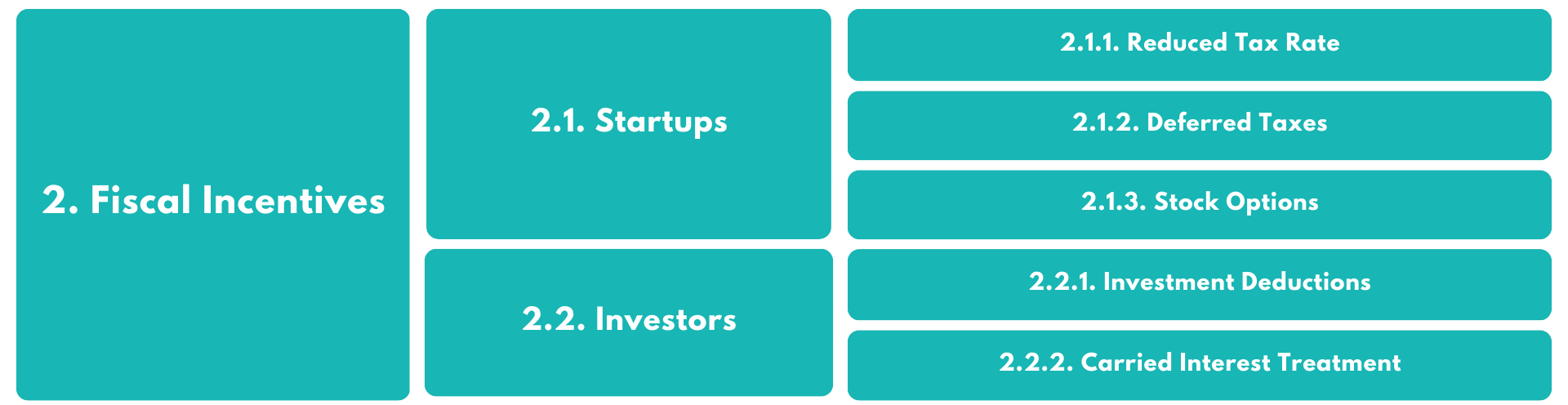

2. Fiscal Incentives

For Startups

1. Reduced Tax Rate

Under the new law, startups benefit from a reduced corporate tax rate for the first four years of positive taxable income.

Reduced corporate income tax rate of 15% for the first four years of profitability, down from the standard 25%.

2. Deferred Taxes

Startups normally suffer during the first years due lack of cash flows. With this new law, they can defer their tax payments for the first two years of positive income without incurring interest, allowing them to manage cash flow more effectively during these critical initial years of operation.

Startups can defer tax payments for the first two positive tax periods, without incurring interest

3. Stock Options

This change encourages startups to use stock options as a means to attract and retain top talent, aligning employee interests with the company's growth.

The tax-exempt amount for stock options provided to employees has been increased from €12,000 to €50,000 annually.

For Investors

1. Investment Deductions

Investors in startups can now enjoy increased deductions:

The deduction rate for investments has been increased from 30% to 50%,

Maximum base rising from €60,000 to €100,000.

2. Carried Interest Treatment

The new law offers favorable tax treatment for carried interest, aligning Spain with other competitive international markets. This makes Spain a more attractive destination for venture capital and private equity funds.

Improved tax treatment for carried interest earned by Venture Capital Partners and Managers, categorizing it as earned income with favorable tax conditions.

3. Regulation

1. Founders and Employees

The new regulations are designed to support both founders and employees by making it easier to recruit and retain skilled workers. This includes simplified visa procedures for international talent, such as the introduction of a digital nomad visa.

Digital Nomad Visa: A new visa allows remote workers to live in Spain for up to one year while working for foreign companies.

Extended Residence Permits: Digital nomads can extend their stay up to three years, with options for renewal and eventual permanent residency after five years.

Beckham Law: The special tax regime has been expanded to include highly qualified professionals, teleworkers, and directors of startups, reducing the prior non-residency requirement from ten to five years.

2. Simplified Processes

Electronic Register (Time and Fees): The process for registering a startup has been streamlined, allowing electronic registration through the CIRCE platform, reducing time required to register a company to just five business days, or six hours if using standard statutes, making the process faster and cheaper,

Simplified Tax ID

(NIE): Notaries can now request tax identification numbers directly for foreign investors, eliminating the need for a Foreign Identification Number (NIE). This simplification reduces administrative hurdles for international founders and investors.

3. ENISA Certification (Downside Point)

One downside of the new law is the requirement for startups to obtain certification from the National Innovation Company (ENISA) to be recognized as a startup and benefit from the new incentives.

This adds an additional step to the process, which can be seen as a bureaucratic hurdle, potentially delaying the time when startups can start enjoying the benefits.

Effects and Comparison with the Previous Law:

Definition of a Startup:

Before: There was no clear and specific definition for startups in Spanish legislation.

Now: The new law defines a startup as a company that is less than 5 years old (7 years for strategic sectors), headquartered in Spain, with at least 60% of its workforce employed in Spain, that does not distribute dividends, and that develops an innovative project with a scalable business model.

Administrative Facilitation:

Before: Administrative procedures were slow and complicated.

Now: A single, electronic point of contact for startup creation has been established, reducing registration times in the Mercantile Registry to five business days, and to six hours if standard statutes are used.

Tax Incentives:

Before: Startups did not have specific tax benefits.

Now: The corporate tax rate is reduced to 15% for the first four years of positive taxable income. Additionally, deductions for investments in startups are expanded, and deferral of tax debt payments in the early years is allowed.

Attracting Talent and Investment:

Before: There were no specific incentives to attract international talent or investment.

Now: A special visa for digital nomads is introduced, and requirements for attracting entrepreneurs and foreign investors are relaxed, including tax exemptions for stock options up to 50,000 euros annually.

Regulation of Treasury Shares:

Before: Limited companies could not acquire their own shares for employee compensation.

Now: Startups are allowed to acquire up to 20% of their own shares for compensation plans, such as stock options, promoting talent retention.

Advantages of the New Law:

Simplification of administrative procedures.

Attractive tax benefits for new businesses.

Incentives to attract and retain foreign talent and investment.

Greater clarity and definition of the legal framework for startups.

Disadvantages:

The need to obtain a certification from ENISA can add an additional step to the process of being recognized as a startup.

Some measures may require adjustments and reviews to ensure their effectiveness and to avoid potential abuses.

Conclusion

The Startup Law 28/2022 positions Spain as a competitive hub for innovation, making it more attractive for entrepreneurs, investors, and highly skilled professionals from around the world. By offering a supportive regulatory and fiscal environment, Spain aims to cultivate a robust and dynamic startup ecosystem.

The new Spanish Startup Law 28/2022 is a significant step towards making Spain a more attractive destination for startups. It addresses many of the challenges previously faced by entrepreneurs, such as high taxes and bureaucratic hurdles

Disclaimer 1: I am not gaining any financial or other personal benefits from announcing or promoting this startups. My purpose is solely to provide information based on the available data.

Disclaimer 2: the information provided is for informational purposes only and does not constitute investment advice. I encourage readers to conduct their own research and due diligence before making any investment decisions.

Thank you for sharing, also in Italy there is something similar